ripple

Product Designer

Responsive Web Design

5 weeks

2026

Microsavings Responsive Web Design

Nearly every participant wanted to save money, but fluctuating income made traditional savings tools feel rigid, overwhelming, and discouraging. Ripple is a responsive savings platform designed to make saving feel flexible, approachable, and achievable through micro-savings, personalized goals, and financial education.

Over five weeks, I led the end-to-end design process from research through usability testing. Research revealed that the real barrier wasn't motivation; it was financial confidence, which became the guiding principle for the product strategy.

How might we help young adults build savings in a way that adapts to their financial limitations while increasing confidence and consistency over time?

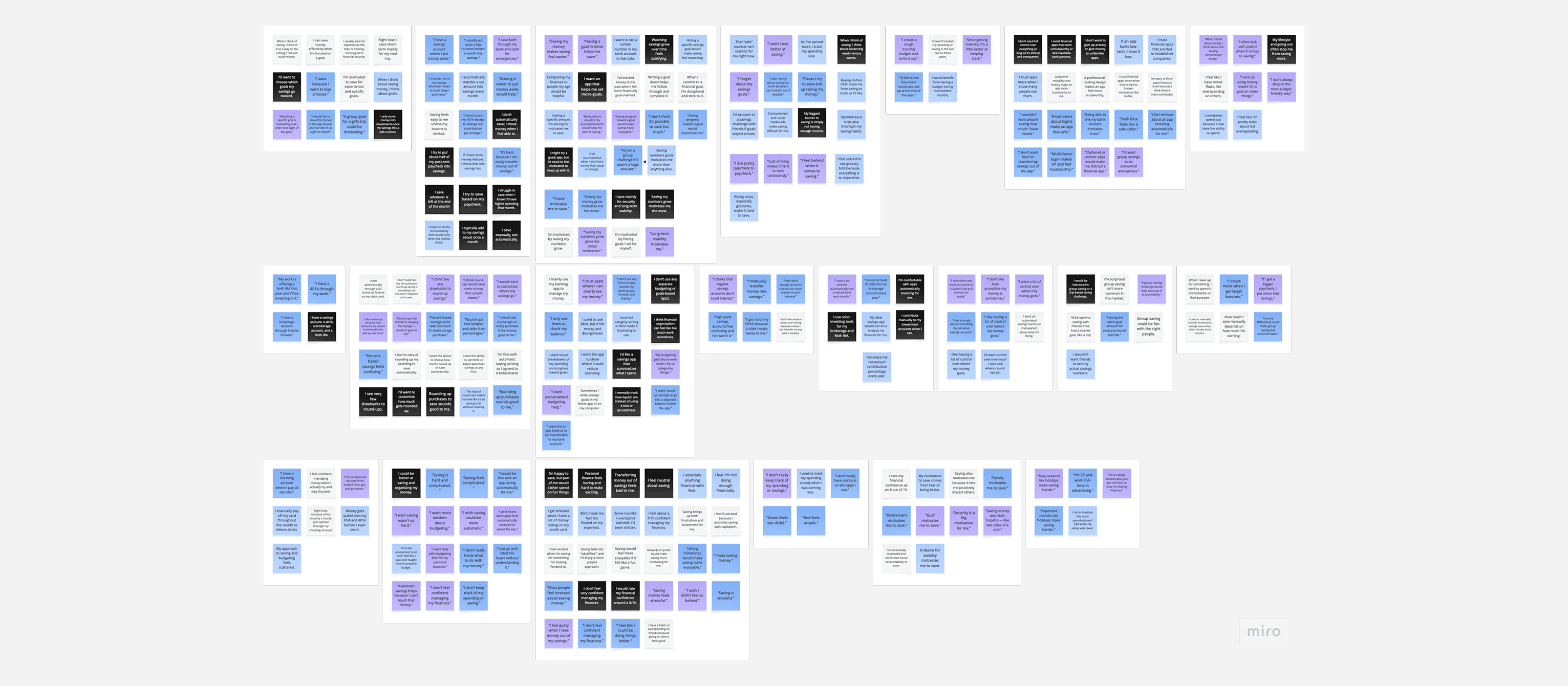

User Research

To gain a deep understanding of users’ saving behaviors, motivations, and pain points, I conducted 5 user interviews, 13 user surveys, and analyzed comparable micro-savings and investment products.

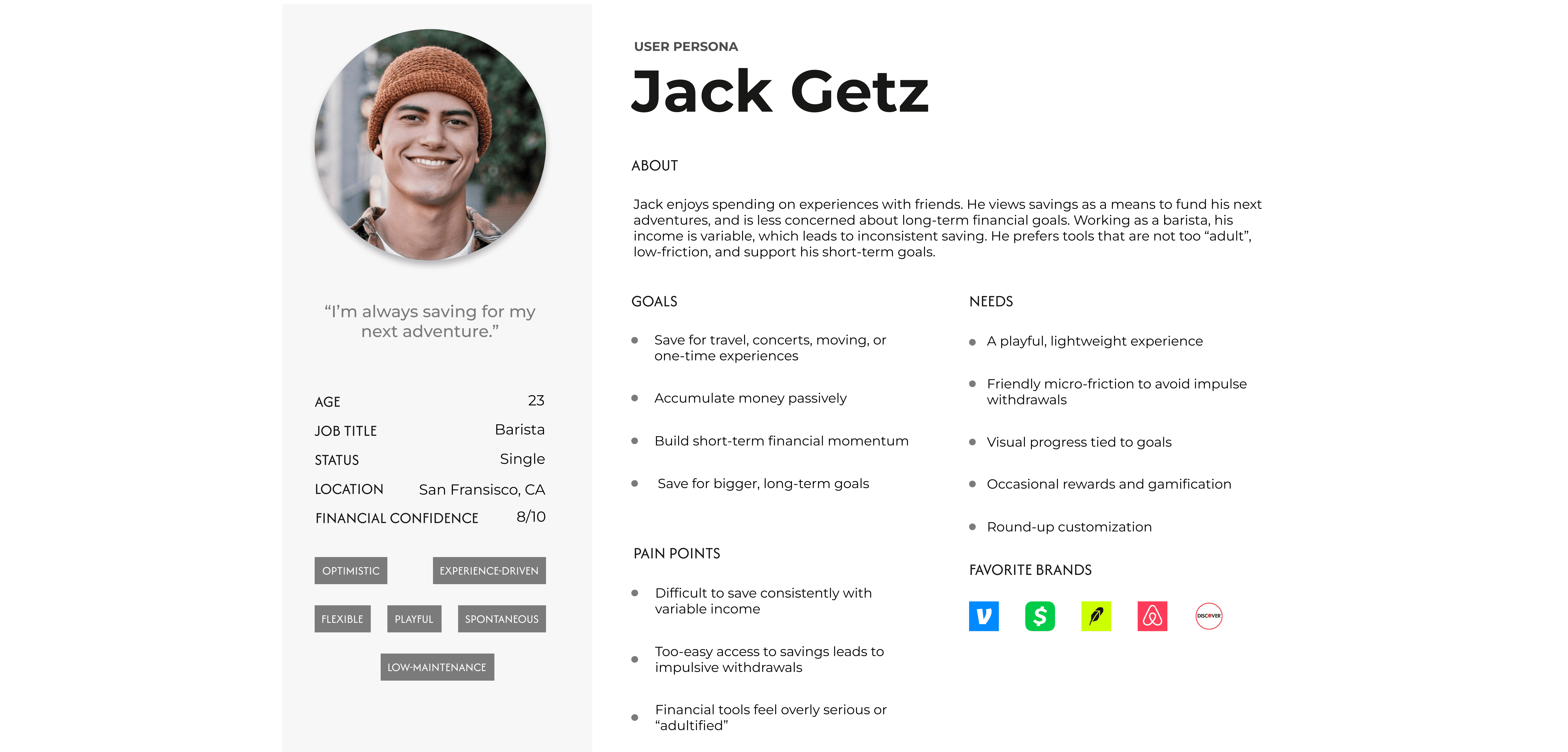

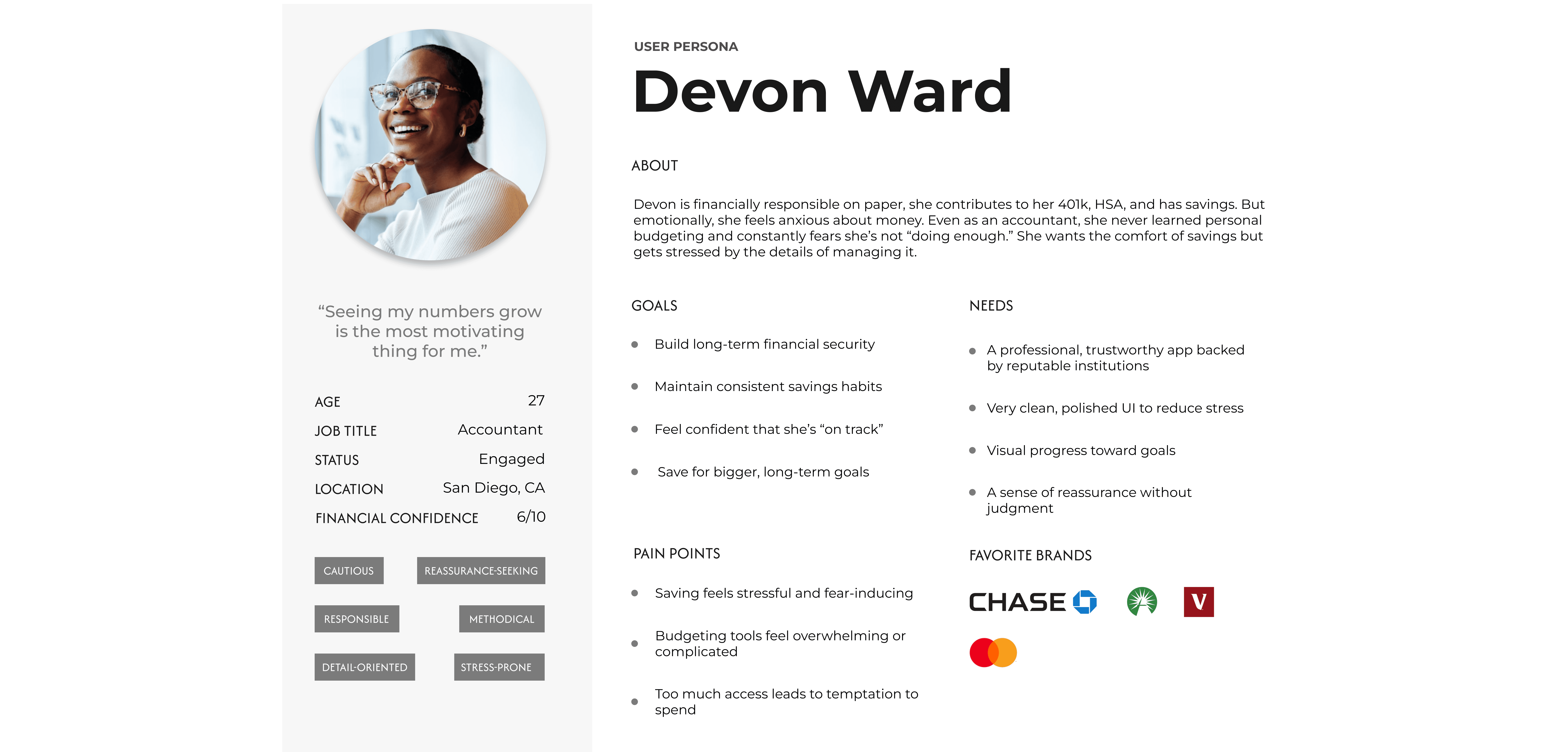

AI-assisted transcription and synthesis tools were utilized to efficiently extract key insights and create an initial affinity map, which I then refined manually to identify patterns, tensions, and areas of opportunity. These insights informed the creation of two personas that grounded design decisions throughout the project.

Key Findings

80% of participants described saving using negative emotions, including stress, fear, guilt, or frustration

80% of participants stated that seeing numbers grow was their strongest motivation to continue saving

100% emphasized the need for:

Adjustable savings amounts

The ability to pause or withdraw at any time

Transparency in where money goes

60% rated their financial confidence at 6 or lower out of 10, even among users actively saving or investing

Participants struggle to save consistently due to income variability, high cost of living, and unexpected expenses

Together, these findings revealed that the challenge wasn't motivating people to save—it was designing a system that felt flexible enough to fit unpredictable financial lives.

Defining the MVP

My initial concept was a comprehensive personal finance platform combining budgeting, investing, debt management, and savings. I believed consolidating financial tools into one place would reduce overwhelm and help users feel more confident. However, research challenged that assumption. I realized I had been designing for comprehensive financial management when what users actually needed was the confidence to take one small step. That insight fundamentally changed the product strategy. Instead of expanding the feature set, I narrowed the MVP around four core experiences: flexible saving, visible progress, transparency, and financial education.

User Journey

Wireframes

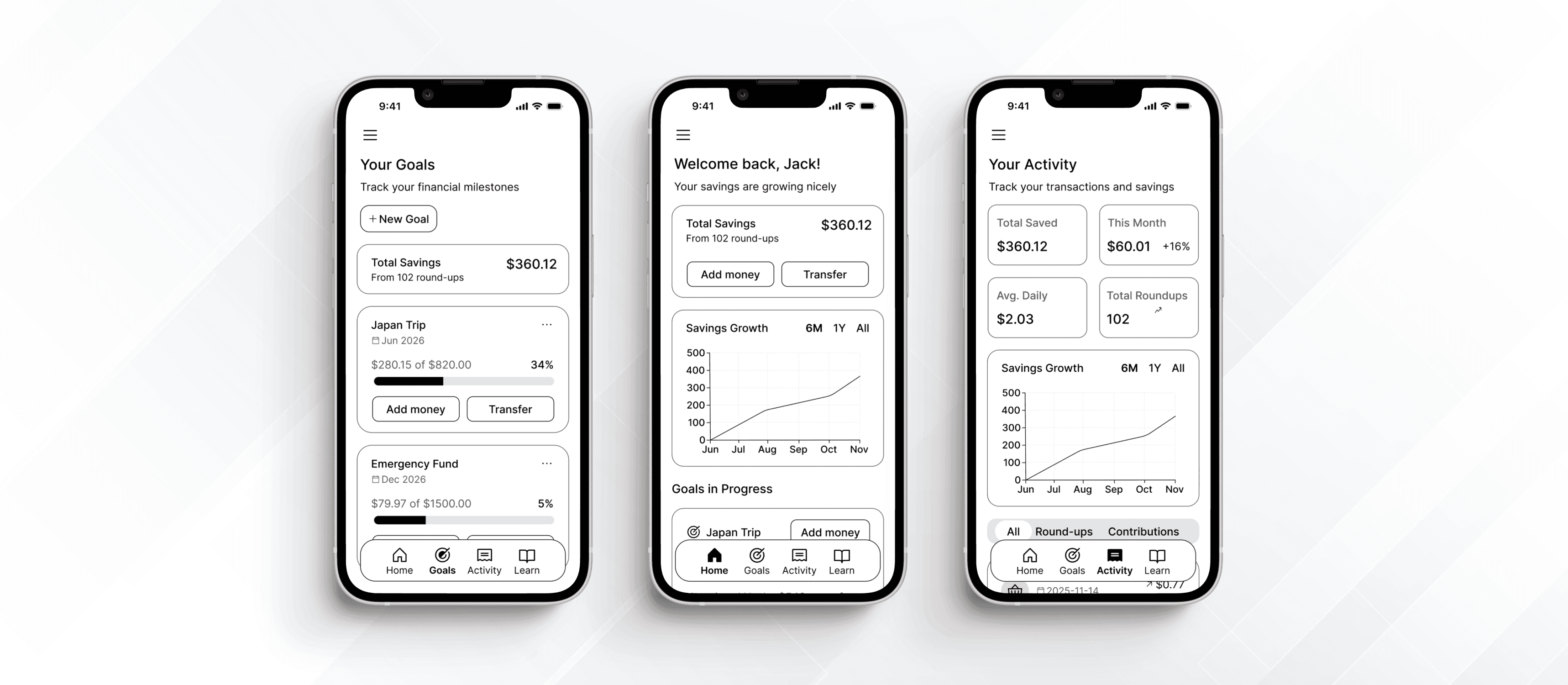

I explored several navigation patterns before settling on a mobile-first dashboard centered around savings progress. Because participants primarily managed finances on their phones, I prioritized quick access to balances, goals, and activity with minimal navigation.

Design System

To create a consistent experience across mobile, tablet, and desktop, I built a responsive design system using reusable components, accessible color contrast, and a scalable typography hierarchy. Designing these foundations early allowed me to iterate quickly during testing while maintaining consistency across breakpoints.

Feature #1: Onboarding

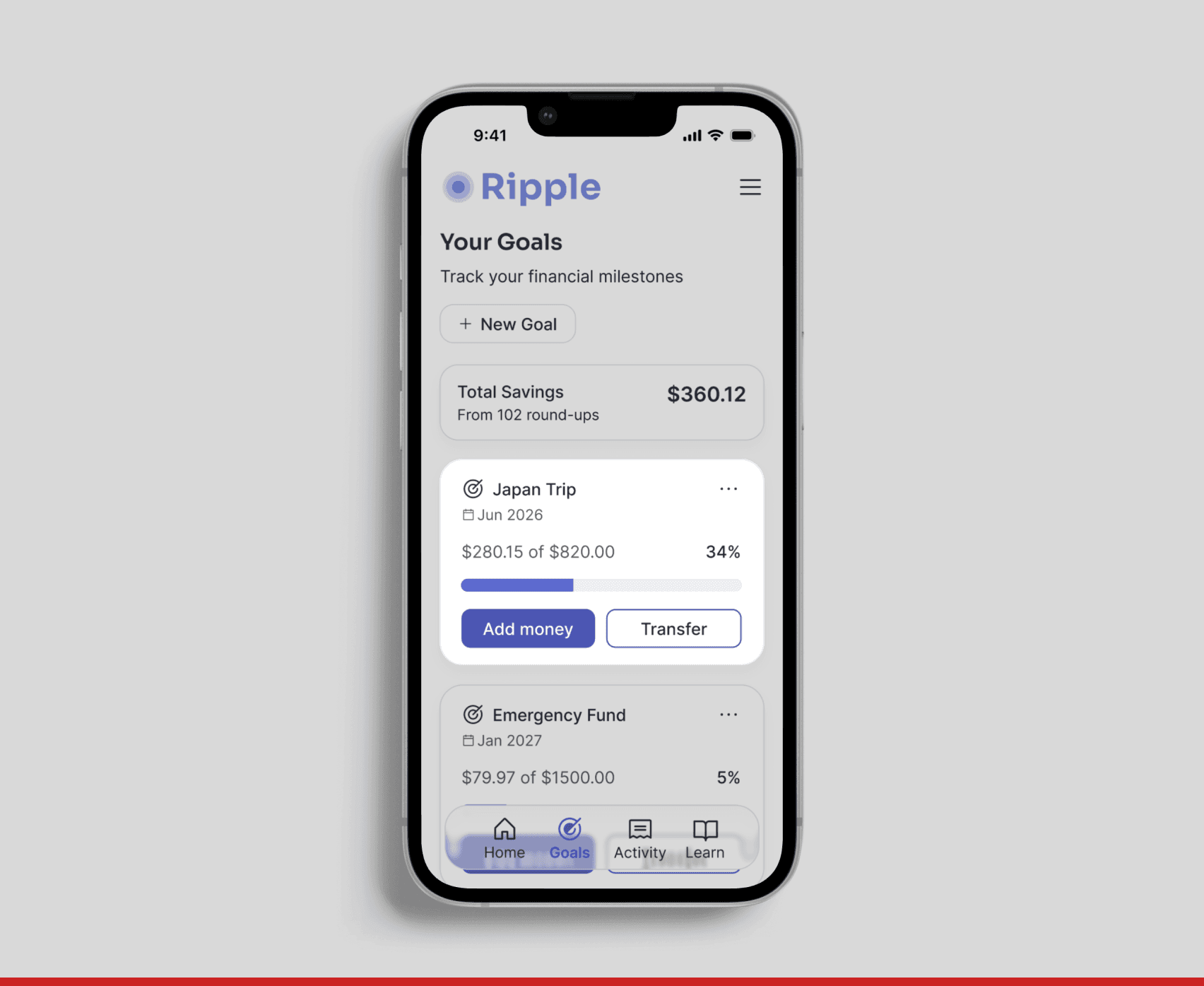

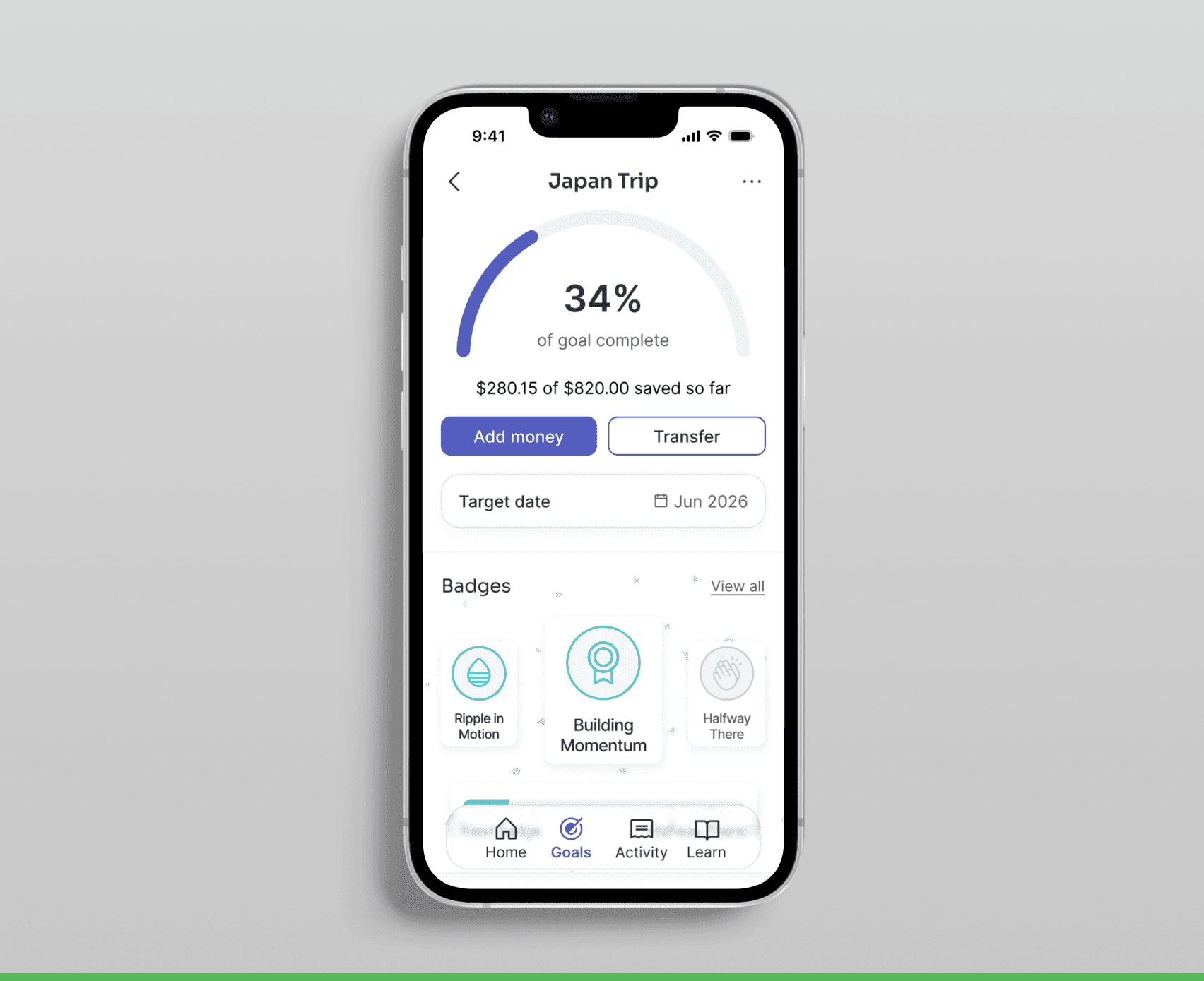

Feature #2: Goals

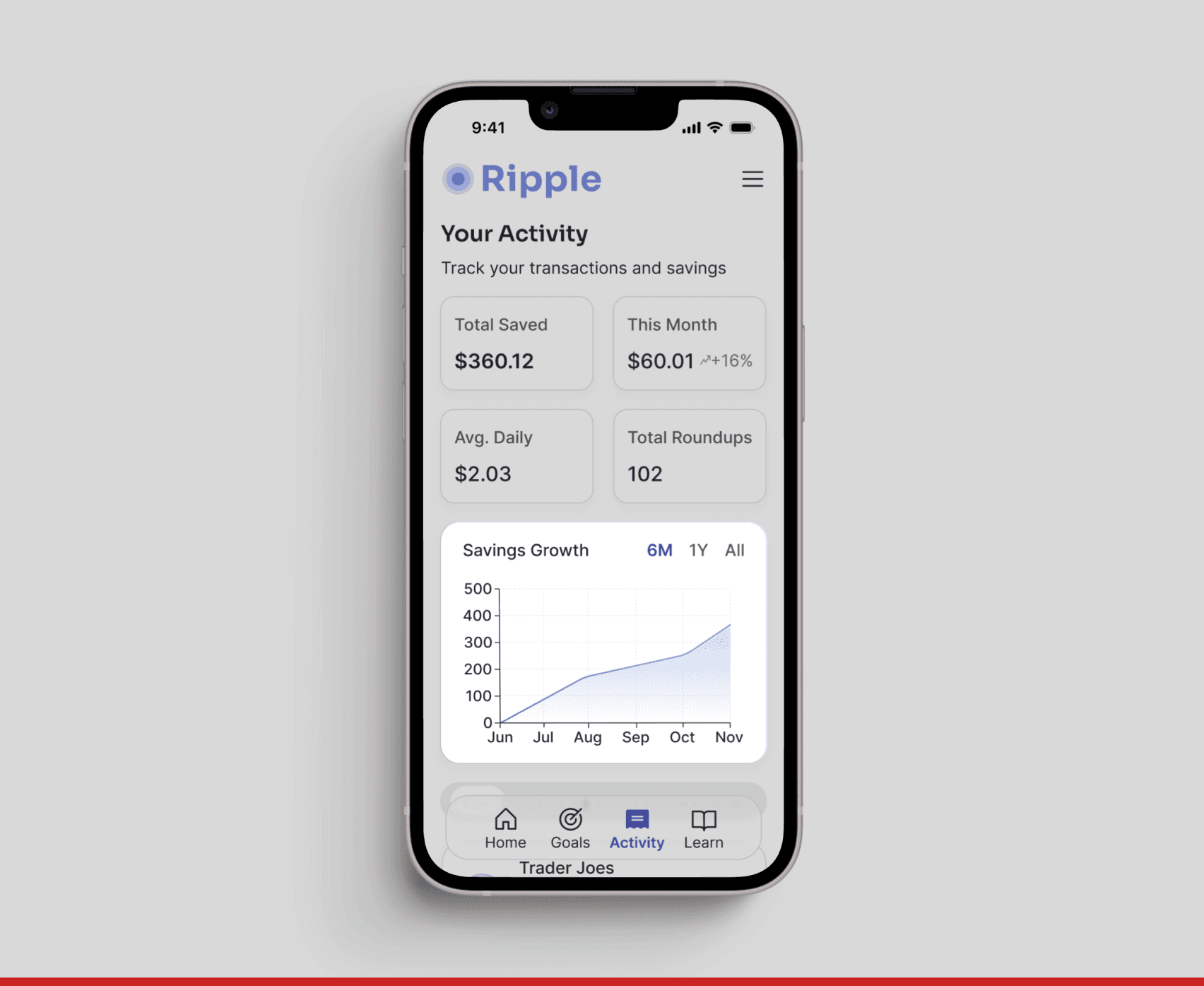

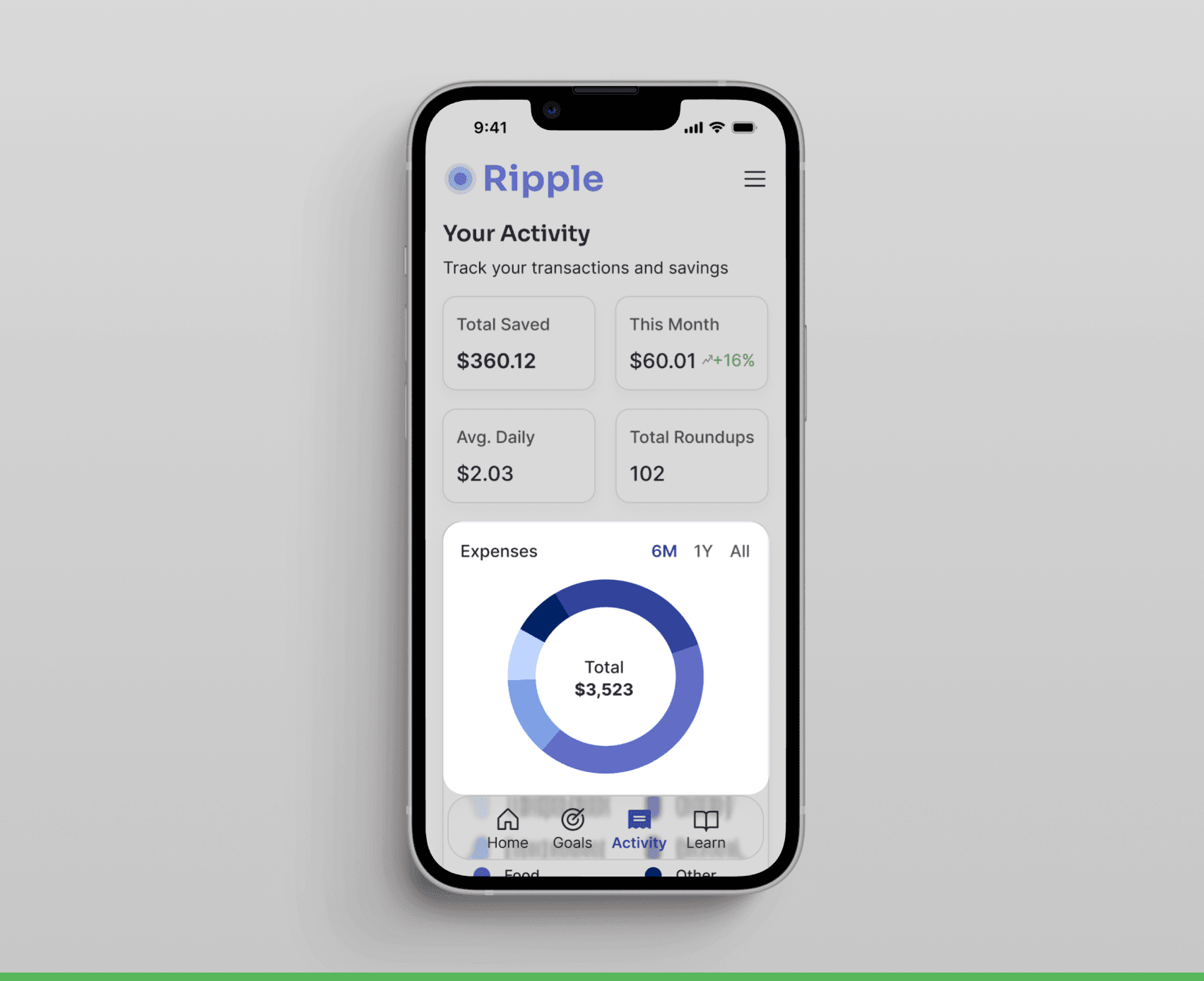

Feature #3: Activity

Feature #4: Learning

Usability Testing

I conducted 5 remote and in-person usability tests to evaluate task clarity, completion rates, and feature comprehension. Key iterations included:

Interactive Prototype

I built a functional prototype to validate core features and responsive design across devices.

Impact